What Is Value?

Imagine, {{Name|friend}}, that you have been playing outside all afternoon and you are really, really thirsty. Someone offers you a choice: a cold glass of water or a shiny diamond ring. Which one do you pick? Right now, in this moment, most people would grab the water!

But wait — diamonds are supposed to be worth way more than water. So what is going on? The answer is that value is not a fixed number stamped on things. Value is how much YOU want something, right now, in your situation. That is the big idea of this lesson.

Here is something interesting. Imagine you have not eaten all day and someone gives you a slice of pizza. Amazing! You would probably love that pizza. Now imagine you already ate five slices and someone offers you a sixth. You might say no thank you.

The pizza did not change. But how much you wanted it changed because you already had a lot of it. Economists call this the law of diminishing marginal utility. That is a fancy phrase that means: the more of something you have, the less each extra piece is worth to you.

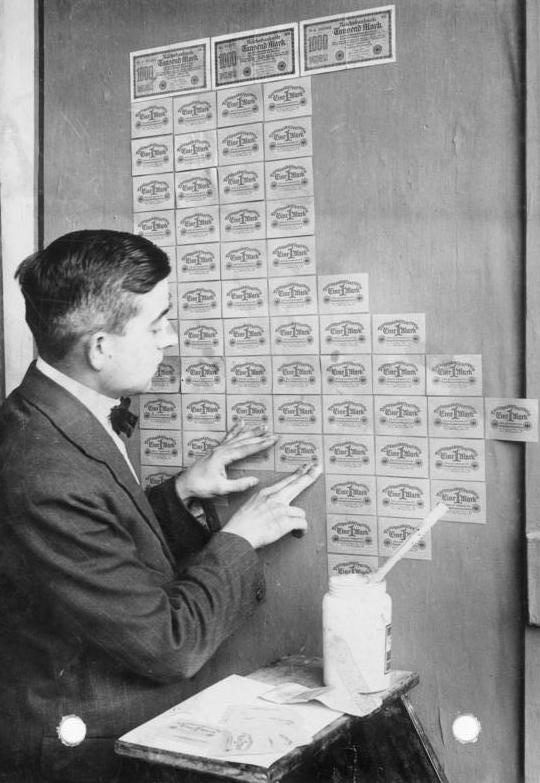

Sometimes governments print so much money that it stops being valuable. This is called hyperinflation. In Germany in 1923, prices doubled every few days. People needed wheelbarrows full of cash just to buy bread. The money had lost its value because there was too much of it.

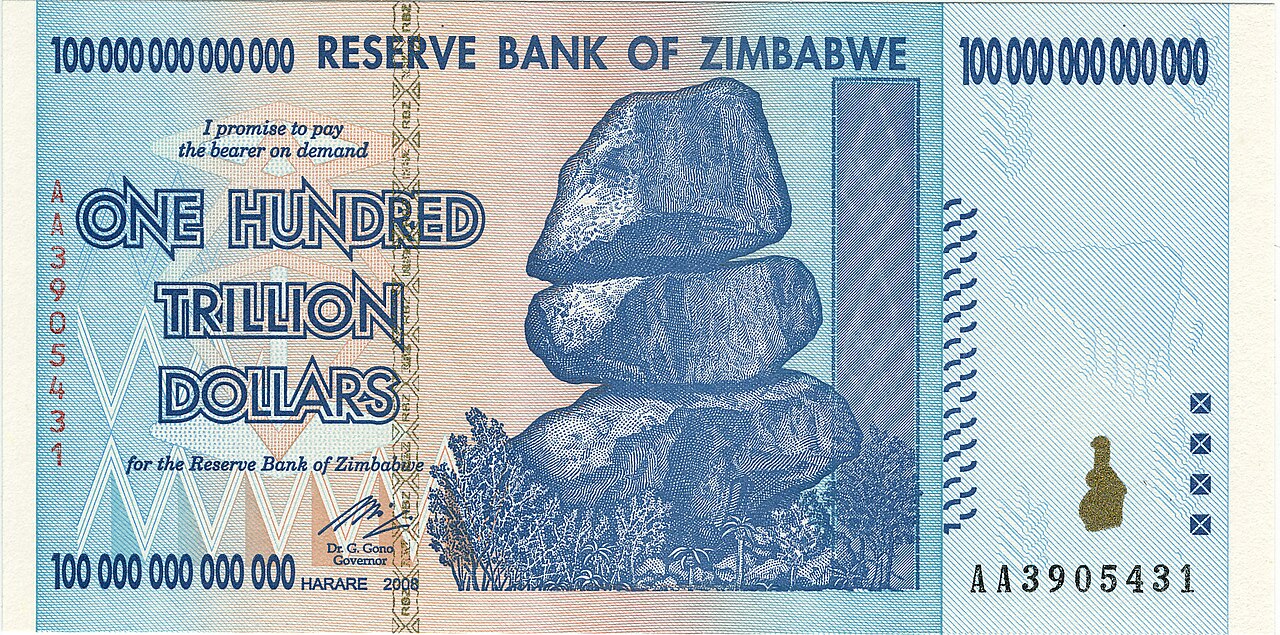

The same thing happened in Zimbabwe and Venezuela more recently. When there is too much of something — even money — each piece of it becomes worth less.

What Is Value?

Imagine, {{Name|friend}}, that you are stranded in the desert, miles from any water. A stranger appears carrying two things: a $10,000 diamond ring and a single bottle of water. He can only carry one of them on his journey and offers to give you whichever one you want. Which do you choose?

Most people, without hesitating, would take the water. But why? A diamond ring is worth thousands of dollars. A bottle of water costs less than two dollars at any gas station. Something important is happening here, and understanding it is the foundation of all economics.

In everyday life, people use "value" and "price" interchangeably. But they are not the same thing. Price is a number, the amount of money agreed upon in a transaction. Value is something deeper: it is how much something matters to a specific person in a specific moment.

Economists identify several sources of value:

For most of human history, economists believed that value was objective, that it existed within the thing itself. A day's labor was worth a day's labor. Gold was worth what it took to mine it. This was called the labor theory of value, and it dominated economic thought for centuries.

Then, in the 1870s, three economists working independently, Carl Menger in Austria, William Stanley Jevons in England, and Léon Walras in France, arrived at the same revolutionary conclusion: value is entirely subjective. It does not exist in objects. It exists in the minds of the people who want them.

The Diamond-Water Paradox

Adam Smith noticed this paradox in 1776: water is essential for survival, yet nearly free. Diamonds are unnecessary luxuries, yet extremely expensive. How could something so vital be so cheap?

The answer is marginal utility, the value of one additional unit. You have access to abundant water. The next glass of water adds very little to your wellbeing. But you likely own zero diamonds. One diamond would be genuinely exciting. Because diamonds are scarce relative to demand, and water is abundant, each additional diamond is worth far more to the average person than each additional glass of water.

If value is subjective, then it follows that two people can look at exactly the same object and see completely different value. This is not irrational, it is the engine that makes trade possible.

Consider three people looking at the same used guitar:

Same guitar. Three radically different values. None of them is wrong, each person is accurately reporting the value it holds for them based on their knowledge, circumstances, and preferences.

The theory of subjective value isn't just an abstract idea in an economics textbook. It governs every financial decision you will ever make.

Why do some people pay $7 for coffee? Because the experience, the ritual, the taste, and the convenience are worth more than $7 to them, even if the raw ingredients cost pennies.

Why does a rare baseball card sell for $50,000 while your neighbor would not pay a dollar for it? Because value is subjective. The collector who knows its history and rarity assigns it enormous value. Someone with no interest in baseball assigns it almost none.

One of the clearest demonstrations of subjective value in history is hyperinflation: the collapse of a currency caused by governments printing money far faster than the economy can produce goods. When the supply of money explodes, the value of each unit collapses. Prices rise so fast that governments must print larger and larger bills just to keep up, until the bills themselves become worthless.

This is not ancient history. It has happened repeatedly across the modern world, and the bills themselves are physical evidence of the collapse.

A History of Collapse: The Largest Bills Ever Printed

The national debt of the United States is the total amount the federal government owes to its creditors. As of 2026 it exceeds $36 trillion and grows by roughly $1 trillion every 100 days.

To put that in perspective: if you spent $1 every second, it would take more than 1.1 million years to spend $36 trillion.

In 2020 alone, the Federal Reserve and US Treasury created roughly $6 trillion of new money in response to the COVID-19 pandemic — adding more dollars to the system in a single year than had existed for most of US history combined.

What does $6 trillion look like in human terms? The median US worker earns about $60,000 per year. So $6,000,000,000,000 ÷ $60,000 = 100 million years of human labor. A typical working life is around 50 years, which means $6 trillion equals roughly 2 million entire human lifetimes of work — created with a keystroke, in twelve months, and handed out before anyone had earned it.

That is the hidden cost of money printing. No one was robbed at gunpoint. But the value of every dollar already earned — every paycheck, every savings account, every retirement fund — was quietly reduced to make room for the new dollars. Economists call this the Cantillon effect: those who receive the new money first spend it before prices rise; everyone else pays for it later, in the form of higher prices on everything they buy.

What Is Value?

From Adam Smith through David Ricardo and Karl Marx, classical economists believed that the value of a good was determined by the amount of labor required to produce it — the labor theory of value. This theory had intuitive appeal: surely things that take more work are worth more? But it could not explain the Diamond-Water Paradox: water requires enormous labor to extract and distribute, yet trades for almost nothing. Diamonds require far less total social labor, yet command extraordinary prices.

The theory also had dangerous political implications. If labor is the source of all value, then profit — the return to capital — is simply unpaid labor extracted from workers. This is exactly the argument Marx made in Das Kapital (1867), and it formed the theoretical foundation for communist economic policy. The collapse of that policy in the 20th century was anticipated, in a sense, by the economists who demolished the labor theory of value a decade before Marx published his masterwork.

In 1871, three economists working independently — Carl Menger in Vienna, William Stanley Jevons in Manchester, and Léon Walras in Lausanne — simultaneously arrived at the same fundamental insight: value is not intrinsic to goods. It is assigned by human minds based on the subjective utility of the marginal unit — the next unit available for consumption.

The key move was the shift from total utility to marginal utility. Water has high total utility — civilization depends on it — but low marginal utility because it is abundant; the next glass available to any individual in a developed society adds almost nothing to their welfare. Diamonds have low total utility but high marginal utility because they are scarce; the first diamond available to a consumer represents a significant addition.

The subjective theory of value has a profound implication that goes beyond individual psychology: prices in a market aggregate the subjective valuations of millions of individuals. No central authority could compute these valuations; they are revealed only through voluntary exchange. This is the foundation of Friedrich Hayek's argument in The Use of Knowledge in Society (1945) that central planning is epistemically impossible: the price system solves a coordination problem that no planned system can replicate.

Hyperinflation episodes — Weimar Germany (1921–1923), Hungary (1945–1946), Zimbabwe (2007–2009), Venezuela (2016–present) — illustrate the subjective theory in extremis. When the supply of money expands faster than the supply of goods, the marginal utility of each monetary unit falls to near zero. The US national debt, now exceeding $36 trillion, raises analogous questions about the long-run marginal utility of dollar-denominated obligations.

Why Things Have Value

You Decide What Things Are Worth

Have you ever traded something with a friend — maybe a snack, a sticker, or a card — and both of you felt happy about it? That is because you each got something you wanted more than what you gave up. Trades like that happen when two people value things differently. And that is totally okay! In fact, it is how all buying and selling works.

Nothing has a value stamped inside it by nature. A baseball card is just cardboard and ink. A piece of gold is just a shiny metal. The reason people pay a lot for rare baseball cards or gold is because many people want them and there are not very many of them. If everyone had a million of the same card, it would not be special anymore.

The Pizza Lesson

Imagine you get one slice of pizza after school. Delicious! Now imagine you get a second slice. Still great. A third slice? Maybe. A fourth? You are getting full. A fifth slice might actually sound bad. The more of something you have, the less you want the next one. Economists have a long name for this: the law of diminishing marginal utility. But you already understood it from the pizza.

This is also why water seems cheap even though we cannot live without it. We have so much water available that one more glass is not very exciting. But if you were lost in a desert, that same glass of water would be worth everything you own. Value changes based on how much you have and how much you need.

When Money Stops Working

Money works because we all agree it has value. But sometimes, when a government prints way too much money, people stop trusting it. In Germany in 1923, prices went up so fast that a loaf of bread cost billions of marks. People used cash as firewood because it was cheaper than buying wood. The money had lost its value — just like that fifth slice of pizza.

The Origins of Value

The Oldest Question in Economics

Long before economists existed, humans faced a puzzle that nobody could fully explain: why do some things cost so much and other things cost so little? Why would a Roman senator pay a year's wages for a rare purple dye, when a common laborer's coat cost almost nothing? Why would a sailor trade weeks of food for a single spice? Why, in a city with no running water, would a glass of water command almost no price, yet in a desert, the same glass could be traded for a horse?

These questions are not merely historical curiosities. They are the same questions you face every time you decide whether something is "worth it", whether to buy a video game, take a job, invest in something, or trade your time for money.

The answers, it turns out, reveal something profound: value does not exist in objects. It exists in people.

The Wrong Answer That Lasted 2,000 Years

For most of human intellectual history, thinkers believed that value was objective, that it existed within things themselves, independent of who was looking at them. The most influential version of this idea was the labor theory of value, which held that the value of something was determined by how much labor went into producing it.

This idea was compelling. If a blacksmith spends ten hours forging a sword, and a potter spends ten hours making a vase, shouldn't they be worth the same? It seemed logical. It was endorsed by Aristotle, refined by medieval scholars, and fully developed by Adam Smith and David Ricardo in the 18th and 19th centuries. Karl Marx later built his entire critique of capitalism on it.

But the labor theory of value was wrong, and a simple thought experiment reveals why.

Now imagine a stranger spends ten minutes sketching a portrait of a famous celebrity. Thousands of people want it.

Which is worth more? The market has an answer: the celebrity sketch. Not because of labor, but because of what people actually want.

The Revolution Nobody Saw Coming

In the 1870s, three economists in three different countries, none aware of the others' work, each arrived at the same revolutionary conclusion almost simultaneously. Carl Menger in Vienna, William Stanley Jevons in Manchester, and Léon Walras in Lausanne each published works that overturned two millennia of economic thought.

Their insight: value is entirely subjective and marginal. It is not an intrinsic property of objects. It is a judgment made by a specific person about a specific unit of a good in a specific circumstance. This came to be known as the Marginal Revolution, and it is the foundation of modern economics.

Solving the Diamond-Water Paradox

The Marginal Revolution finally solved a puzzle that had stumped Adam Smith himself, now called the Diamond-Water Paradox.

Water is absolutely essential for human life. Without it, you die in days. Yet water is cheap, sometimes free. Diamonds are utterly unnecessary for survival. Yet they sell for thousands of dollars per carat. How can something so vital cost so little, while something so frivolous costs so much?

The answer lies in marginal utility combined with scarcity. In most circumstances, water is abundant. You already have access to hundreds of gallons. One more glass adds almost nothing to your wellbeing. Your marginal utility for water is nearly zero.

Diamonds, however, are scarce. Most people own none. One diamond would represent a significant addition to their holdings. The marginal value of one diamond is therefore high.

Value, Trade, and Why Both Sides Win

Once you understand that value is subjective, a remarkable consequence follows: voluntary trade always creates value for both parties.

Think about it. If you and I trade, it's because I value what you have more than what I'm giving up, and you value what I have more than what you're giving up. We both walk away better off in our own estimation. Nobody lost. Value was created, not transferred.

This is one of the most counterintuitive and important ideas in economics. People often think of trade as a zero-sum game, that one person's gain must be another's loss. The theory of subjective value reveals this is wrong. Every voluntary exchange generates a "surplus" of satisfaction for both parties. This is why trade, specialization, and markets have made human civilization exponentially wealthier over time.

As You Read, Mark:

Subjectivism and the Price System

The Epistemics of Price

A price is not merely a number. It is a compressed signal encoding the aggregate subjective valuations of every buyer and seller in a market. When the price of lumber rises sharply after a hurricane, no central authority needs to issue instructions to builders to economize on wood, to loggers to work overtime, to architects to redesign using substitute materials. The price does all of this automatically, coordinating the behavior of people who know nothing of each other across thousands of miles.

This is the insight Friedrich Hayek formalized in 1945, but it rests entirely on the subjectivist value theory established by Menger, Jevons, and Walras in 1871. If value were objective — if goods had intrinsic worth independent of human preferences — then in principle a sufficiently intelligent planner could calculate correct prices. The subjectivist position closes this door permanently: preferences are private, heterogeneous, and continuously changing, and cannot be aggregated by any mechanism other than the market itself.

Menger's Insight: Goods and Wants

Carl Menger's Grundsätze der Volkswirtschaftslehre (1871) introduced a systematic account of value that begins not with production costs but with human wants. A thing becomes an economic good only when four conditions hold: a human need exists; the thing has properties that make it capable of satisfying that need; the person recognizes this connection; and the person has sufficient command of the thing to direct it toward satisfying the need. This seemingly simple framework has enormous implications: value is always relational, always perspectival, always tied to a specific person in a specific situation.

Menger also distinguished between goods of different orders: consumers' goods that directly satisfy wants, and producers' goods (capital) that satisfy wants indirectly by producing other goods. The value of capital goods is imputed backward from the value of the consumer goods they produce — a point that would later anchor the Austrian theory of capital and business cycles.

Hyperinflation as a Value Experiment

Hyperinflation episodes are, in an important sense, natural experiments in the subjective theory of value. When the Weimar Republic's Reichsbank expanded the money supply to finance reparations payments in 1921–1923, the marginal utility of each additional mark approached zero faster than the presses could print them. By November 1923, the exchange rate reached 4.2 trillion marks per dollar. The Hungarian hyperinflation of 1945–1946 remains the most extreme on record, with prices doubling every 15 hours at its peak. In each case, the lesson is identical: the value of money is not guaranteed by the government that issues it. It is maintained only by the continued subjective confidence of the people who use it.

What Is Value?

What Is Value?

Draw a line or write the letter of the correct definition next to each term.

Who is most likely to buy it? Who is least likely? Explain how subjective value and marginal utility determine each person's decision.

What Is Value?

Let's Talk About It

Seminar: What Is Value?

This guide is organized into four levels of thinking, from recall through debate. You do not need to cover every question. A good seminar picks 3–5 questions and goes deep rather than covering all 12 shallowly.

Seminar: Subjectivism and Its Consequences

Trade & Specialization

Think about everything you used today. Your breakfast, your clothes, your shoes, your phone or computer. Did your family make any of those things? Probably not! You got them by trading — your family earned money at work, and used that money to buy things other people made.

This is trade. And it works because different people are good at different things. A farmer grows food really well. A shoemaker makes shoes really well. When they trade with each other, both of them end up with more than if each tried to do everything alone.

A long time ago, before money existed, people traded things directly. A farmer might trade ten apples for a pair of shoes. This is called barter.

But barter has a big problem. What if the shoemaker does not want apples? What if he wants wheat? Then the apple farmer cannot get shoes unless he first finds someone who has wheat AND wants apples. This gets very complicated very fast!

A man named Adam Smith watched workers in a pin factory and noticed something amazing. One worker trying to make a pin from scratch could make maybe one pin per day. But ten workers, each doing just one step of the job, could make 48,000 pins per day!

Why? Because when you do the same thing over and over, you get very good at it very fast. You waste no time switching between tasks. This is called the division of labor.

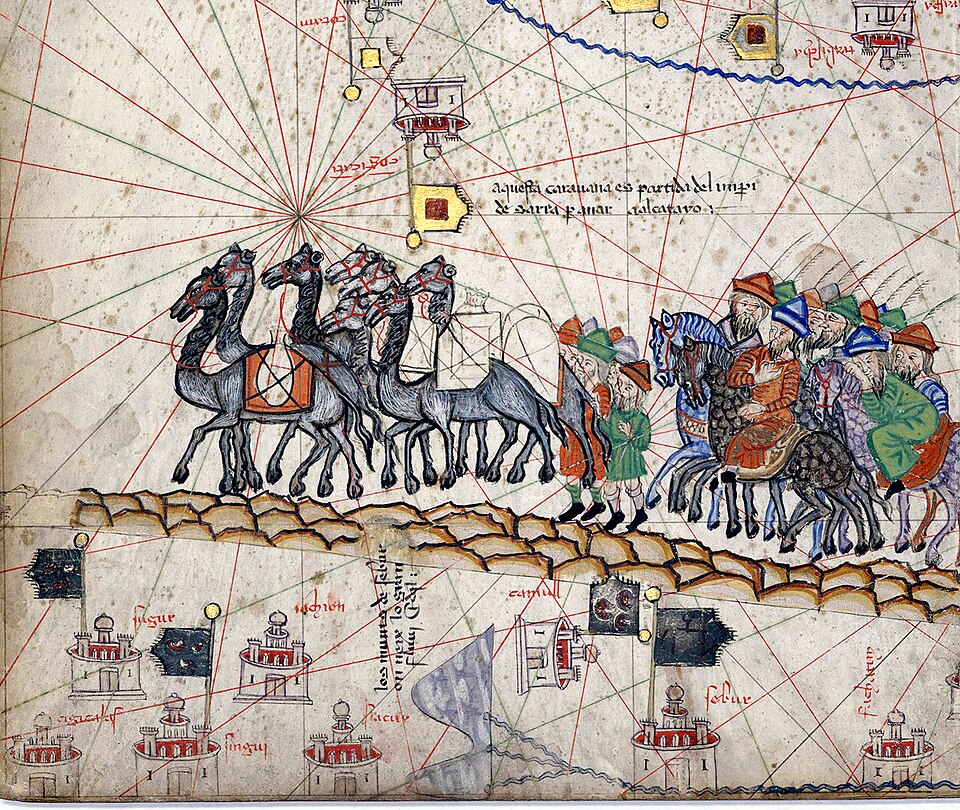

People have been specializing and trading for thousands of years. Here are three snapshots of how it has looked.

Trade & Specialization

Try, {{Name|friend}}, to build a pencil from scratch. Not buy one. Build one. You would need to harvest cedar wood from a forest, mine and smelt graphite, extract rubber from a rubber tree in South America, gather brass for the ferrule, and manufacture the yellow paint from petroleum-based compounds. No single person on earth knows how to do all of this, let alone has access to all the materials.

Yet a pencil costs less than twenty-five cents. The economist Leonard Read made this point brilliantly in his 1958 essay I, Pencil: no single person can make a pencil, yet the market produces billions of them cheaply and efficiently. The reason is specialization and trade.

Before money existed, people traded directly: fish for grain, labor for shelter, tools for cloth. This is called barter. It works reasonably well in small communities where everyone knows each other and needs overlap.

But barter has a fundamental problem that economists call the double coincidence of wants. For a trade to happen, you must find someone who has exactly what you need and wants exactly what you have, at the same time. In a village of twenty people this is manageable. In a city of millions it is nearly impossible.

Specialization means focusing your efforts on producing the things you do best, and relying on trade to obtain everything else. Even if one person is better than everyone else at everything, it still pays for them to specialize. This is the idea of comparative advantage, one of the most important and counterintuitive ideas in all of economics.

It was first clearly described by David Ricardo in 1817. His insight: even if Portugal could produce both wine and cloth more efficiently than England, both countries would be better off if Portugal focused on wine (where its advantage was greatest) and England focused on cloth. Total output rises. Both countries gain from trade.

Most people intuitively think of trade as a zero-sum exchange: one person gains what the other loses. This is wrong. Voluntary trade creates wealth because both parties value what they receive more than what they give up.

Combined with specialization, the effect multiplies. When each person produces what they are relatively best at and trades for the rest, total output rises for everyone. This is not a theory. It is demonstrated every time you visit a grocery store, hire a contractor, or buy anything made in another country.

Three snapshots of specialization and exchange — from a medieval caravan to a modern container port.

Trade & Specialization

Ricardo's principle of comparative advantage, published in 1817, remains one of the most counterintuitive and empirically robust results in all of economics. The intuitive case for trade — that parties should exchange when each has an absolute advantage in producing something the other needs — understates the argument dramatically. Even when one party is better at producing everything, both parties still gain from specializing in their respective comparative advantages.

The formal statement: a producer should specialize in the good for which their opportunity cost is lowest relative to trading partners, regardless of absolute productivity. This holds at the level of individuals, firms, regions, and nations. The gains from trade do not require any party to be deficient — they arise from the inescapable mathematics of relative scarcity and opportunity cost.

The empirical record on trade and prosperity is unusually clear by the standards of social science. The periods and regions of greatest economic growth have consistently coincided with the expansion of trade networks: the Pax Romana, the Hanseatic League, the post-1945 GATT/WTO trading order. Countries that liberalized trade — South Korea, Taiwan, Singapore, China — experienced the fastest sustained rises in living standards in recorded history. Countries that pursued import substitution and self-sufficiency — India pre-1991, much of Latin America in the 1970s — consistently underperformed.

This does not mean trade has no distributional consequences. It does. The gains from trade are diffuse — spread across millions of consumers in the form of lower prices — while the losses are concentrated among specific industries and workers who face import competition. This asymmetry explains why trade generates political resistance even when its net economic effect is positive.

Three concrete instances of the same mechanism — specialization plus voluntary exchange — expanding total output across very different eras.

The Amazing Pencil

Can You Make a Pencil?

Try this experiment: think about everything it would take to make a simple wooden pencil from scratch. You would need to cut down a cedar tree. You would need to mine graphite from the ground. You would need to get rubber from a rubber tree that only grows in certain parts of the world. You would need brass for the little metal ring, and yellow paint made from chemicals.

No single person on earth knows how to do all of that. Yet pencils cost about twenty-five cents. How is that possible?

The answer is trade and specialization. Thousands of people each do their small part: the logger, the miner, the chemist, the factory worker, the truck driver. None of them set out to make a pencil. They were just doing their job. But together, through trade, they made something none of them could make alone.

Why Does Specializing Help?

When you do one thing over and over, you get really good at it. A chef who makes pasta every day gets much faster and better than someone who only makes it once a year. A carpenter who builds furniture all day becomes much more skilled than a person who tries to build a chair once.

This is why it makes sense for different people to do different jobs. When everyone specializes and then trades, there is more of everything for everyone.

A World Without Trade

Imagine if every family had to make everything it needed itself. You would have to grow your own food, sew your own clothes, build your own house, and make your own tools. You would have almost nothing, and life would be very hard.

Trade is what allows the modern world to exist. It is what puts food in grocery stores, phones in pockets, and books on shelves.

The Miracle of Trade

Nobody Makes Anything Alone

Consider, {{Name|friend}}, the shirt you are wearing. Someone grew the cotton. Someone else harvested it, spun it into thread, wove it into fabric, cut it, sewed it, packaged it, shipped it, and stocked it on a shelf. The dye came from a chemical plant. The buttons from a factory. The thread from another. The truck driver who delivered it relied on a truck built by hundreds of engineers, running on fuel refined from oil drilled from the ground by workers on the other side of the world.

No single human being made your shirt. Thousands did. And none of them knew you existed. They were all simply specializing in what they do, trading their output for money, and using that money to obtain what they need. The result, multiplied across billions of people, is the modern economy.

This is the miracle of trade: anonymous strangers, each pursuing their own interests, cooperating through the price system to produce outcomes that no central planner could design or coordinate.

Barter and Its Limits

Long before money, people traded directly. Archaeologists have found evidence of barter networks stretching thousands of miles in the ancient world, with obsidian from volcanic islands trading for shells from distant coasts. In small communities, barter worked. Everyone knew everyone. Needs were simple. The range of goods was limited.

But as societies grew, barter became increasingly impractical. The core problem is the double coincidence of wants: for a barter trade to happen, both parties must want exactly what the other has, at exactly the same time. In a society of thousands of specialized producers, the odds of this alignment become vanishingly small.

This friction is not merely inconvenient. It is economically crippling. When people cannot easily trade their output for the inputs they need, specialization breaks down. People are forced to be generalists, producing a little of everything rather than becoming excellent at anything. Total output falls. Everyone is poorer.

Ricardo and Comparative Advantage

The English economist David Ricardo published On the Principles of Political Economy and Taxation in 1817, introducing one of the most important and genuinely surprising ideas in economics: comparative advantage.

The intuitive case for trade is easy: if one country is better at making wine and another is better at making cloth, they should each make what they are best at and trade. Ricardo showed something far less obvious: even if one country is better at producing both wine and cloth, trade still benefits both countries. The key is not absolute advantage but comparative advantage: which activity has the lower opportunity cost for each producer.

The Division of Labor

Adam Smith opened The Wealth of Nations in 1776 with a celebrated description of a pin factory. A single worker attempting every step of pin production might make one pin per day. But ten workers, each specializing in one of the eighteen distinct operations required, could produce 48,000 pins per day: an increase in output of roughly 48,000 percent.

Smith identified three reasons why the division of labor increases productivity so dramatically: workers become more skilled through repetition, no time is lost switching between tasks, and specialization makes it easier to invent machines that automate each step.

Every modern industry is built on this foundation. The hospital, the restaurant, the software company, and the construction firm all function through radical specialization and the coordination of specialized labor through trade.

Trade and Prosperity

The evidence that trade creates prosperity is overwhelming. The periods and places in human history with the most open trade have consistently produced the greatest increases in living standards. The Pax Romana, which enabled trade across the Mediterranean world, produced centuries of relative prosperity. The opening of global trade routes in the 15th and 16th centuries transformed European economies. The industrial revolution was accompanied by a dramatic expansion of both domestic and international trade.

In the modern era, countries that have embraced open trade, including South Korea, Taiwan, Singapore, and China, have experienced the fastest rises from poverty in recorded history. Countries that have restricted trade and attempted self-sufficiency have almost universally seen their citizens grow poorer.

The Division of Knowledge

Beyond Division of Labor

Adam Smith's pin factory illustration captured something real but incomplete. The gains from specialization are not merely about repetition and skill-building — they are fundamentally about the division of knowledge. As economies grow more complex, the relevant scarce resource is not labor or capital but expertise: the accumulated know-how that makes production possible at all.

This is the insight behind Leonard Read's celebrated 1958 essay I, Pencil. Read's point was not simply that pencil production involves many workers. It was that no single mind contains — or could contain — the knowledge required to coordinate the entire supply chain. The cedar forester in Oregon knows nothing of the graphite mines in Sri Lanka. The chemical engineer who formulates the lacquer has no knowledge of rubber cultivation in the Amazon. Yet the pencil exists, cheaply and reliably, because the price system coordinates these dispersed knowledge fragments without any central direction.

Hayek's Extension

Friedrich Hayek formalized this insight in his 1945 paper "The Use of Knowledge in Society." Hayek distinguished between scientific knowledge — general principles that can be written down and transmitted — and what he called "knowledge of the particular circumstances of time and place." The latter includes the local businessman who knows which warehouse has excess stock, the trader who senses a shift in regional demand before any statistic captures it, the worker who knows which machine is about to break.

This dispersed, tacit, unteachable knowledge is what makes markets work. The price of lumber rising in one region signals to distant suppliers to ship more, without anyone needing to understand why. Specialization does not merely increase productivity — it generates and concentrates the kind of knowledge that no central authority could replicate or replace.

The Ricardian System and Its Limits

Ricardo's comparative advantage model assumes static production technologies and factor immobility. In practice, comparative advantage is dynamic: countries can change what they are good at through investment, education, and industrial policy. South Korea had no semiconductor industry in 1960 and is now among the world's leaders. This required deliberate government intervention that the simple Ricardian model would not recommend.

The tension between static comparative advantage (trade what you currently produce best) and dynamic comparative advantage (invest to produce what you want to be best at) is one of the central unresolved debates in development economics. Neither free traders nor industrial policy advocates have a complete answer.

Trade & Specialization

Trade & Specialization

Write the letter of the correct definition next to each term.

Trade & Specialization

Let's Talk About It

Seminar: Trade & Specialization

Seminar: Trade & Its Discontents

Needs, Wants & Opportunity Cost

A need is something you must have to survive — food, water, shelter, clothing to stay warm. A want is something you would like but could live without — video games, candy, a new bike.

Neither needs nor wants are bad. But understanding the difference helps you make better decisions about money. When you spend money on a want before taking care of your needs, you can get into trouble.

Here is something most people never think about: every time you choose to do something, you are also choosing NOT to do something else. That "something else" you gave up is called the opportunity cost.

If you spend Saturday playing video games, the opportunity cost might be the homework you did not finish, the exercise you skipped, or the time with a friend you missed. The game did not cost you just time — it cost you everything else you could have done with that time.

A long time ago, a man named Bastiat told a story about a broken window. A boy breaks a shop window. Some people say this is actually good because the glass repairman will get paid! But Bastiat said: wait. The shopkeeper now has to spend money fixing the window — money he was going to spend on a new suit. The tailor gets nothing. The town is not richer. It just lost a window.

This story teaches us to always ask: what else could that money or time have been used for? That is the hidden cost — the thing you do not see.

Sometimes a whole country has to choose between needs and wants. These photos show what that looks like.

Needs, Wants & Opportunity Cost

{{Name|Friend}}, you wake up on a Saturday with a completely free day. You could sleep until noon. You could work a shift at your part-time job and earn $60. You could study for next week's exam. You could spend the day with a friend who is moving away. You could finish a book you have been meaning to read for months.

You cannot do all of these things. You must choose. And here is the key insight: whatever you choose, you are simultaneously choosing not to do everything else. The value of the best alternative you gave up is the true cost of your decision. Economists call this the opportunity cost.

Economists draw a basic distinction between needs and wants. A need is something required for survival and basic functioning: food, water, shelter, clothing adequate for the climate, basic healthcare. A want is anything beyond that: a specific food, a comfortable house, fashionable clothes, entertainment, luxury.

This distinction matters because it helps us understand where scarcity bites hardest. Resources spent on wants are resources not spent on needs, and in poor societies this tradeoff is life and death. In wealthy societies the line blurs, which creates its own set of problems around priorities, debt, and consumption.

The concept of opportunity cost is deceptively simple and profoundly important. Every time you make a choice, you give up the next-best alternative. The value of that foregone alternative is your opportunity cost.

Opportunity cost is not always money. When you spend an evening watching television, the opportunity cost might be the studying you could have done, the exercise you skipped, or the sleep you lost. When a government spends money on roads, the opportunity cost is the hospitals, schools, or tax relief it did not fund instead. When a business invests in new equipment, the opportunity cost is the dividend it could have paid shareholders or the research it could have funded.

Because all choices involve opportunity costs, all meaningful decisions involve tradeoffs. A tradeoff is simply the recognition that gaining more of one thing requires giving up something else. Understanding tradeoffs clearly is the foundation of rational decision-making.

Economists use a tool called the production possibility frontier to visualize tradeoffs at a national scale. It shows all the combinations of two goods an economy can produce with its available resources. Producing more of one good necessarily means producing less of another. There is no free lunch.

Three moments when whole societies had to face their opportunity costs out loud.

Opportunity Cost & Rational Choice

The concept of opportunity cost is not merely a useful heuristic — it is the definitional foundation of rational decision-making under scarcity. Every resource, including time, money, attention, and labor, has alternative uses. The true cost of any choice is not its price tag but the value of the best foregone alternative. This means that even activities with zero monetary cost — sleep, leisure, volunteering — have real economic costs that a rational actor must account for.

Opportunity cost explains phenomena that confuse purely monetary accounting. Why do highly paid professionals hire others to perform tasks they could do themselves? Because their time has high opportunity cost. Why do countries import goods they could produce domestically? Because the opportunity cost of domestic production exceeds the import price. Why does the sunk cost fallacy cause such widespread irrationality? Because people confuse historical expenditures — which cannot be recovered — with future opportunity costs, which are the only costs that matter for forward-looking decisions.

Bastiat's broken window parable is not merely a lesson about property damage. It is a general methodological principle: good economic analysis requires accounting for both visible effects and invisible counterfactuals. Every government program, subsidy, tax, or regulation produces visible benefits — the jobs created, the industry supported, the services provided — and invisible costs — the resources diverted from alternative uses, the innovations that did not occur, the industries that did not develop.

This principle applies directly to some of the most contested policy debates of our era. When a government subsidizes domestic manufacturing, the seen effect is employment in that sector. The unseen is the higher-cost inputs for all downstream industries, the foregone imports that would have freed resources for higher-value activities, and the tax burden on other sectors. Bastiat's framework does not resolve these debates — the magnitudes matter — but it identifies what must be estimated before any conclusion is justified.

In ordinary times, opportunity costs are diffuse and largely unseen — exactly Bastiat's point. In crises, governments make them explicit. Three examples below.

The Cost You Cannot See

The Story of the Broken Window

A long time ago, a French writer named Bastiat told a story. A shopkeeper's son accidentally breaks the shop window. Everyone is upset at first. But then someone in the crowd says: "Actually, this is good! Now the glass repairman will get paid. He will spend that money at other shops. The whole town benefits!"

Does that make sense to you? It sounds nice, but Bastiat said it was wrong. Here is why: the shopkeeper was going to spend that money anyway — maybe on a new suit. Now the tailor gets nothing. The town did not gain anything. It just lost a perfectly good window.

The lesson: when you see something, always ask — what did not happen because of this? What was the hidden cost?

The Saturday Problem

Imagine you wake up Saturday morning with a completely free day. You can sleep in, study for a test, earn money helping a neighbor, hang out with a friend, or finish a book. You cannot do all of them. Whatever you pick, you are giving up everything else.

The most valuable thing you did not do is called the opportunity cost. If you sleep in and miss earning $20, that is your opportunity cost. If you study and miss seeing your friend, that is your opportunity cost. There is no escape from it — every choice means giving something up.

Nothing Is Truly Free

People often say things like "free samples," "free shipping," or "free public school." But nothing is truly free. Someone always pays — maybe the store, maybe taxpayers, maybe you with your time. The economist Milton Friedman said it simply: "There is no such thing as a free lunch." Even a free lunch costs someone something.

The Seen and the Unseen

The Broken Window

In 1850, the French economist Frédéric Bastiat published a short essay that remains one of the most powerful illustrations of economic reasoning ever written. It is called The Parable of the Broken Window.

A shopkeeper's son accidentally breaks a shop window. A crowd gathers. Someone in the crowd argues that this is not actually a bad thing. The glazier who replaces the window will earn money. He will spend that money on shoes. The shoemaker will spend it on bread, and so on. The broken window has stimulated economic activity. The town is richer for it.

Bastiat's response was devastating: this argument only considers what is seen, the glazier's new income, and ignores what is unseen. The shopkeeper would have spent that money on something else, perhaps a new suit. The tailor would have received the income instead. The town is no richer. It is exactly as rich as before, minus one window.

Needs, Wants, and the Problem of Scarcity

Every economy in human history has faced the same fundamental problem: resources are finite while human wants are effectively unlimited. This gap is what makes economics necessary. If everything were abundant and free, there would be no need for prices, tradeoffs, or allocation decisions.

The distinction between needs and wants helps clarify where resource allocation decisions are most consequential. When resources are so scarce that basic needs cannot be met, every allocation decision is potentially life or death. When basic needs are met and the question shifts to wants, the stakes are lower but the decision-making is no less important for individual wellbeing and financial health.

The economist Abraham Maslow proposed a hierarchy of needs in 1943, arguing that humans prioritize needs in a predictable order: physiological survival first, then safety, then social belonging, then esteem, and finally self-actualization. While psychologists debate the details, the basic insight is useful for economics: until lower-order needs are met, higher-order wants receive little attention or resources.

Opportunity Cost in History

The concept of opportunity cost is not just an abstract idea. It has shaped the outcomes of empires, wars, and civilizations.

When Rome chose to expand its military during the late Republic and early Empire, the opportunity cost was investment in trade, infrastructure, and governance. Historians debate whether the enormous resources devoted to military conquest, which produced short-term wealth through plunder and tribute, ultimately weakened the institutions needed for long-term prosperity.

When the Ming dynasty of China chose in the 15th century to restrict maritime trade and destroy its ocean-going fleet after the voyages of Zheng He, the opportunity cost was the trade networks, technological exchange, and economic growth that followed European maritime expansion. China turned inward precisely when the world was opening up.

These are macro examples, but the principle operates at every scale. Every dollar a government spends on one program is a dollar not spent on another. Every hour you invest in one skill is an hour not invested in a different one.

Sunk Costs and the Trap of the Past

One of the most common and costly mistakes in decision-making is letting past expenditures influence current choices. A sunk cost is a cost that has already been incurred and cannot be recovered, regardless of future decisions. Rational decision-making requires ignoring sunk costs entirely.

You have already paid $15 to see a movie that turns out to be terrible. Should you stay to "get your money's worth"? No. The $15 is gone either way. The real question is: given where you are right now, is staying in this theater for two more hours the best use of your time? Almost certainly not. The money is a sunk cost. Only the future costs and benefits are relevant.

Making Better Decisions

Understanding opportunity cost and avoiding sunk cost thinking are two of the most practical skills economics offers. Together they encourage a forward-looking, clear-eyed approach to decisions: ask not what you have already spent but what the best use of your resources is right now.

This applies to money, time, attention, and energy. Every hour spent on social media has an opportunity cost in reading, exercise, skill development, or sleep. Every dollar spent on a depreciating luxury good is a dollar not compounding in an investment. Recognizing these tradeoffs does not mean living ascetically. It means making choices consciously rather than by default.

Bastiat, Hazlitt, and the Economics of the Unseen

The One Lesson

Henry Hazlitt's 1946 book Economics in One Lesson opens with a claim: the whole of economics can be reduced to a single lesson, and that lesson is Bastiat's. "The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups."

Hazlitt's book is a systematic application of Bastiat's seen-and-unseen framework to a range of economic policies: tariffs, minimum wages, rent control, farm subsidies, public works programs. In each case, the argument has the same structure. The policy produces a visible, concentrated benefit for an identifiable group. It produces an invisible, diffuse cost spread across the rest of the economy. Political attention focuses on the former; economic analysis requires accounting for both.

The Production Possibility Frontier

The production possibility frontier is the economist's formal representation of opportunity cost at a national scale. It shows all combinations of two goods an economy can produce using its available resources and technology. Moving along the frontier — producing more guns and fewer butter, or vice versa — has a direct opportunity cost: each additional unit of one good requires sacrificing some amount of the other.

Points inside the frontier represent inefficiency — resources not fully used. Points outside are unattainable given current constraints. The frontier shifts outward with technological progress, capital accumulation, or workforce expansion. Every policy debate about resource allocation is, ultimately, a debate about where on the frontier a society should operate — and whose preferences should determine the answer.

Sunk Costs and the Concorde Fallacy

The Concorde supersonic passenger jet is one of the most celebrated examples of the sunk cost fallacy in public policy. By the mid-1970s, it was clear the aircraft would never be commercially viable. The development cost was unrecoverable. Rational analysis required asking: given where we are today, does the expected future revenue justify the future costs? The answer was no. But Britain and France continued the program for decades, unable to walk away from the billions already spent.

Economists call this the "Concorde fallacy." It afflicts individuals (staying in bad relationships because of invested time), businesses (continuing failing products because of development costs), and governments (continuing wars because of lives already lost). The rational response in every case is the same: ignore sunk costs entirely, evaluate only future costs and benefits, and make the forward-looking decision that maximizes expected value from this point onward.

Needs, Wants & Opportunity Cost

Needs, Wants & Opportunity Cost

Needs, Wants & Opportunity Cost

Let's Talk About It

Seminar: Needs, Wants & Opportunity Cost

Seminar: The Seen and the Unseen

What Is Wealth?

Imagine someone wins a million dollars in the lottery. They have never saved money before. They have never learned how to invest. They do not know how to run a business. What do you think happens?

Studies show that many lottery winners spend all their money within a few years and end up back where they started — or worse. Why? Because they had money but not wealth. Wealth is not just the money you have. It is the skills, knowledge, habits, and relationships that help you create and keep value over time.

Economists think about wealth in four main categories:

The lottery winner had financial wealth but lacked human and social capital. Without those, the money disappeared.

Here is something important: wealth is not a fixed pie. When a farmer grows wheat, she creates new wealth. When a developer builds software that a million people use, he creates new wealth. When you develop a skill and use it to help others, you create new wealth.

This means that for someone to become wealthier, they do not need to take from someone else. They can create something new. This is how the world has become so much richer over the past 200 years.

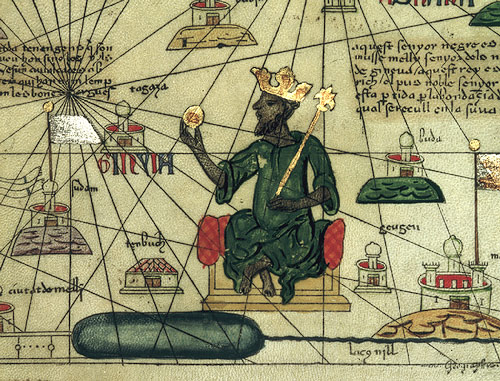

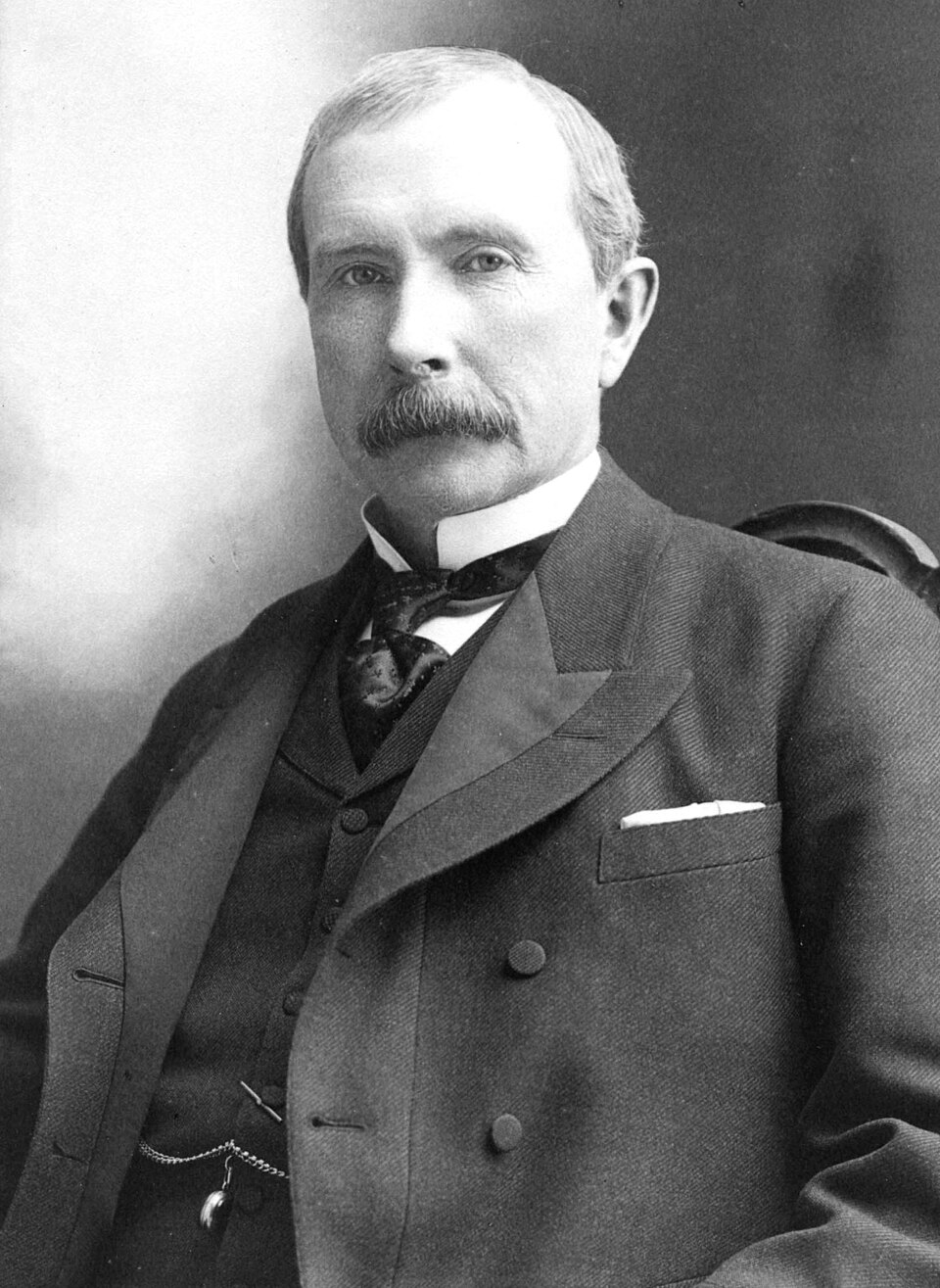

Wealth has taken very different forms over the centuries — gold, land, skills, networks, factories. Here are three people history remembers as wealthy, for very different reasons.

What Is Wealth?

Studies of lottery winners consistently show the same surprising result: within a few years, most have returned to roughly the same level of financial wellbeing they had before winning. A significant number end up worse off. Some go bankrupt. Research on large lottery winners has found that the sudden influx of money, without the knowledge, habits, relationships, and skills that normally accompany wealth, tends to dissipate quickly.

This tells us something important: money is not the same as wealth. A person can receive millions of dollars and end up poorer for it. Another person can earn a modest income and build substantial wealth over decades. What makes the difference?

Money is a tool. It is a medium of exchange, a unit of account, a store of value. Its purpose is to facilitate trade and preserve purchasing power. Wealth is something deeper: it is the sum of all valuable things you own or control, including things money cannot directly buy.

Adam Smith titled his most famous work The Wealth of Nations, not "The Money of Nations." The distinction was deliberate. A nation with vast gold reserves but no productive capacity, no skilled workers, no working infrastructure, is not wealthy. A nation with few natural resources but highly educated workers, strong institutions, and productive businesses can be extremely wealthy.

One of the most important economic insights is that wealth is not fixed. It can be created. This seems obvious, but its implications are profound and frequently misunderstood in public debate.

The world of 1800 was not wealthy by modern standards. The average person in England in 1800 had roughly the same material standard of living as the average person in ancient Rome. Then, within 200 years, average living standards in developed nations increased by a factor of roughly 30 to 50 times. This was not redistribution. New wealth was created through productivity, specialization, trade, technological innovation, and capital accumulation.

Understanding the forms of wealth points toward how to build it. Financial wealth is built through earning, saving, and investing. Physical wealth through acquiring and maintaining productive assets. Human capital through education, skill development, and experience. Social capital through building genuine relationships and a reputation for reliability and integrity.

The most resilient forms of wealth are those least dependent on any single government, currency, or institution. A person whose only wealth is cash savings in one currency is exposed to monetary policy and inflation. A person whose wealth is diversified across skills, relationships, productive assets, and multiple forms of financial capital is far more resilient.

Three people history remembers as wealthy — for three very different reasons. Notice which forms of capital each one really depended on.

What Is Wealth?

The naive definition of wealth — the quantity of money or goods held at a point in time — is inadequate for several reasons. A country can have enormous monetary reserves and be desperately poor, as Venezuela's experience illustrates. An individual can receive a large windfall and be financially worse off within years, as lottery research documents. The quantity of money held is not the determinant of wealth; it is the symptom of underlying productive capacity.

A more rigorous definition: wealth is the accumulation of claims on future value production. Financial assets represent claims on the earnings of enterprises. Physical capital represents productive capacity. Human capital represents the ability to generate economic value through skilled labor. Social capital represents the network of relationships and institutions that reduce transaction costs and enable coordination. All four are components of wealth, and the relationships between them are as important as their individual quantities.

Deirdre McCloskey's three-volume project on the "Bourgeois Era" argues that the Great Enrichment — the 3,000 percent increase in real income per person in market economies over two centuries — cannot be explained by capital accumulation, natural resources, institutions, or geography alone. Her claim is that the crucial variable was ideological: a change in the social attitudes toward innovation, trade, and entrepreneurship that occurred in northwestern Europe between approximately 1600 and 1800.

This is a controversial thesis, but it highlights something important: the conditions for wealth creation are not purely material. They include the legal institutions that protect property rights, the cultural norms that honor productive activity, the educational systems that develop human capital, and the social trust that enables large-scale cooperation among strangers. Where these conditions are absent, physical resources generate what economists call the "resource curse" — the paradox of mineral-rich countries with chronically poor populations.

Three historical fortunes, each leaning on a different blend of the four capitals. The lesson is not who was richest — it's which capitals their wealth was actually built on, and what happened when those capitals were withdrawn.

Two Neighbors

A Story About Two Neighbors

Sam and Alex both earn $50,000 per year. After ten years, Sam has $150,000 saved and invested, owns his home, and has learned valuable new skills at work. Alex has $500 in savings, $30,000 in credit card debt, and earns the same salary he did ten years ago.

Same income. Very different results. What made the difference? It was not luck. It was the choices each person made about how to spend their time and money — and how much they invested in themselves.

The Four Kinds of Wealth

Financial wealth is money — savings, investments, stocks. Sam built this by spending less than he earned and investing the rest.

Physical wealth is things that have lasting value — a house, tools, equipment. Sam owns his home; Alex rents and has nothing to show for years of payments.

Human wealth is your skills and knowledge. Sam took courses and got better at his job. Alex did not. So Sam earns more now.

Social wealth is your network — the people who know and trust you. Sam built relationships at work and in his community. When an opportunity came up, people thought of him.

The Most Important Kind

Of all four kinds of wealth, human capital may be the most important. Here is why: no one can take your skills from you. A bank can fail. A house can burn down. But what you know and can do travels with you everywhere, through any crisis.

This is why reading, learning, and practicing skills now — even before you have much money — is one of the best investments you can make in your future.

What the Wealthy Know

Two Neighbors, Same Income

Consider, {{Name|friend}}, two neighbors who both earn $60,000 per year. After ten years, one has $200,000 in savings and investments, owns their home outright, has developed marketable skills that have increased their earning power, and maintains a strong professional network. The other has $2,000 in savings, carries $40,000 in debt, and earns the same $60,000 they did a decade ago.

Same income. Radically different wealth. What explains the difference? It is not luck, though luck plays a role. It is not intelligence alone. The difference lies in decisions, habits, knowledge, and the understanding of what wealth actually is and how it is built.

This course is designed to give you the knowledge that separates these two outcomes. The most important thing to understand first is that wealth is built, not received. It is the result of deliberate choices about how to allocate time, money, attention, and relationships over long periods of time.

The Great Enrichment

For most of human history, economic growth was nearly imperceptible. Historians estimate that average living standards barely changed between ancient Rome and medieval Europe, roughly 1,500 years of near-stagnation. Then something changed.

Beginning in roughly the 18th century in northwestern Europe, and accelerating through the 19th and 20th centuries, average living standards began rising at an unprecedented rate. The economic historian Deirdre McCloskey calls this the Great Enrichment: a 3,000 percent increase in real income per person in countries that adopted market institutions, the rule of law, and reasonably open trade.

This was not redistribution. There was no fixed pool of wealth that was divided more generously. Entirely new wealth was created through productivity, specialization, technological innovation, and capital accumulation. The question of how this happened, and why it happened in some places and not others, is one of the most important questions in all of economics.

Human Capital: The Invisible Asset

The economist Gary Becker won the Nobel Prize in 1992 partly for his work on human capital, the idea that investments in education, training, and health produce measurable economic returns, just as investments in machinery and buildings do.

Becker's insight was that people are not merely workers or consumers. They are also investors in themselves. Every hour spent developing a skill, every book read, every difficult project undertaken, is an investment that pays returns for decades. The return on human capital investment is often higher than the return on financial investment, particularly early in life when skills compound over many working years.

This has important implications for how you think about education, career choices, and how you spend your time. A teenager who spends two hours per day developing a marketable skill is making an investment that will likely outperform any financial return available to them at that age.

Social Capital and the Hidden Network

The sociologist Robert Putnam documented in his influential book Bowling Alone (2000) how the decline of community associations, civic organizations, and neighborhood networks in America has eroded social capital across income levels. His research showed that communities with high social capital, the dense webs of relationships and mutual trust that come from active participation in civic life, consistently outperformed low-social-capital communities on economic outcomes, health, and educational attainment.

The practical implication is straightforward: your network is part of your wealth. Not in the cynical sense of using relationships purely for financial gain, but in the genuine sense that trust, reputation, and reciprocal relationships create economic value that cannot be manufactured with money alone.

Protecting What You Build

Wealth that is built can also be eroded. The most common threats are inflation (which reduces the purchasing power of financial wealth), taxation, debt, and poor decisions. Understanding these threats is as important as understanding how to build wealth in the first place.

Historically, the forms of wealth most resilient to erosion have been human capital (skills and knowledge), diversified productive assets, and strong relationships. Pure financial wealth stored in a single currency or a single institution has proven repeatedly vulnerable to government policy, economic disruption, and monetary debasement.

Capital, Institutions, and Development

Becker and the Economics of Human Capital

Gary Becker's 1964 book Human Capital applied the tools of microeconomics to a domain previously considered outside economics: the decision to invest in education, training, and health. Becker's insight was straightforward but consequential: people invest in themselves for the same reason they invest in equipment — to increase future productive capacity and thus future income.

This framework has profound implications. If human capital investment follows the same logic as physical capital investment, then the return on education can be estimated, compared across alternatives, and optimized. It also implies that the conventional distinction between "spending" on education and "investing" in machinery is misleading — both are investments in productive capacity, differing mainly in the form of the asset created.

Putnam and the Decline of Social Capital

Robert Putnam's 2000 book Bowling Alone documented a dramatic decline in social capital across American communities since the 1960s. Civic organization membership, neighborhood association participation, church attendance, informal socializing — all declined substantially. Putnam's analysis showed that this decline was correlated with worse outcomes across a range of economic and social metrics: lower educational attainment, higher crime, worse health outcomes, reduced economic mobility.

The economic mechanism is through trust and coordination. High-social-capital communities have dense networks of reciprocal relationships that reduce transaction costs — the friction involved in every economic exchange. When you trust your neighbors, you can hire local contractors without elaborate contracts, lend tools without collateral, and build businesses on handshake agreements. Where social capital is low, every transaction requires more legal infrastructure, more verification, more enforcement — all of which consume resources that could go to productive activity.

McCloskey and the Ideological Origins of Prosperity

Deirdre McCloskey's argument in The Bourgeois Virtues and its sequels is that the conventional explanations for the Great Enrichment — capital accumulation, trade, technology, institutions — are insufficient. All of these things existed in many societies before the Industrial Revolution without producing comparable growth. What was different in 18th-century Britain and the Netherlands was a change in what McCloskey calls "rhetoric": the social dignity and ethical legitimacy accorded to commercial activity and innovation.

When merchants and inventors were regarded as honorable contributors to society rather than as parasitic opportunists, the pool of talent flowing into productive commercial activity expanded enormously. The resulting explosion of innovation — the steam engine, textile machinery, the factory system — was not caused by capital alone but by the liberation of human ingenuity that ideological change permitted.